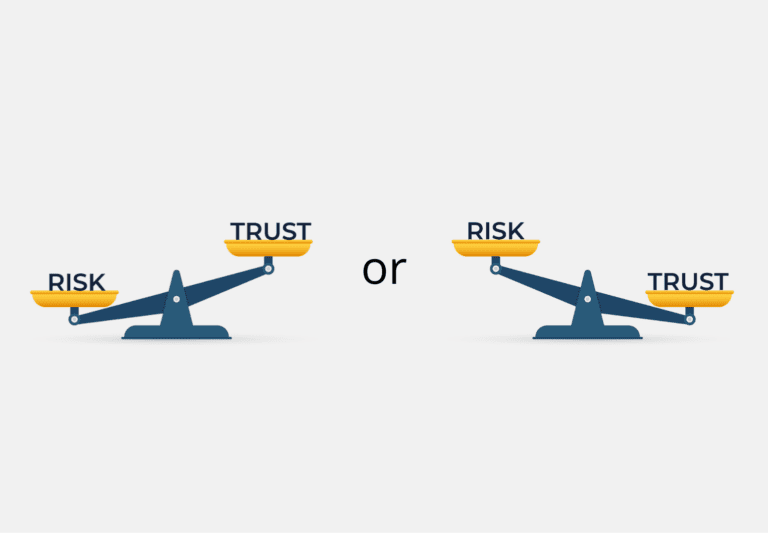

Financial requirements differ from one service to another regarding conditions, timing, currency, accompanying documents, and payment methods. These factors are determined by the deal’s equilibrium between trust and risk.

Transforming Modern Trade Finance

This article will present the various payment methods available and in what circumstances to do so. For brevity, we’ll refer mainly to banks, but NBFIs often play the same role in transactions.

How to choose a Trade Finance Instrument

When there exists some risk, and the trust level is not high, a seller often prefers to involve a trusted third-party bank to supervise the deal’s workflows. This adds trust to the agreement and formalizes it, imposing various terms and conditions.

Payment often involves a transfer of documents and requires a document management process, which, like the payment process itself, can be managed either by the bank or individually between sellers and buyers.

Payment Instruments

When is Telegraphic Transfer used?

-

- 1. When the payment method is managed by banks.

-

- 2. When there is no trust between parties, the seller might demand the entire payment transaction pre-production by TT. In this case, the documents’ envelope is transferred directly between the parties when the seller receives the payment.

- 3. When there is complete trust between parties and no need for involvement by banks. In this case, the payment process begins once an invoice is submitted, and the envelope of documents is transferred directly between the parties.

Cash Against Documents (CAD):

When is Cash Against Documents used?

- 1. When the seller has some concerns about the deal and can’t be certain, the buyer will complete their side of the transaction.

Letter of Credit (LC):

When is a Letter of Credit used?

- 1. When transaction risk is high, and there is no trust between parties. It is also a financing solution and means to reduce political risk.

Timing of Payment

Payment timing options

-

- 1. Pre-production

- 2. Pre-delivery

- 3. Post-delivery

- After the cargo is released from customs

As we have seen, the terms and conditions of a sale, specifically the payment method, the payment timing and documents required, are determined according to the level of risk and trust between parties. WAVE BL enables sellers and buyers to digitize the document exchange process, cut courier costs and paper expenditures, and ultimately reduce the cost of trade. Banks and non-banking financial institutions that offer trade finance solutions similarly benefit from rapidly issuing and transferring documents while expediting verification and improving the customer experience.